Even subsidies and unproven technology aren’t enough to make West Susitna coal power make sense.

The coal with carbon capture plant is an expensive false solution dependent on inaccurate economic analysis, massive state subsidies, and experimental technology.

These days in Alaska, it’s fashionable to claim any project you want to build will solve both the Cook Inlet Gas crisis and climate change. The West Susitna coal plant idea claims to do both, and would actually do neither.

Instead, it’s an extremely expensive power source that tries to justify itself by ignoring the costs of transmission and the West Susitna Access Road and comparing its cost to inaccurate and inflated prices for natural gas power. Also it fails to compare to cheaper renewable options, and uses overly optimistic assumptions for both coal plant costs and experimental carbon capture technology. Rosy presentations with bad math have led the Mat Su borough assembly to pass a resolution stating “Coal-fired power generation with CCUS presents a compelling alternative to imported LNG by providing affordable, reliable, clean electricity to the Railbelt grid at substantially lower than current costs” -- when nothing could be further from the truth.

There are a lot of things left out of those rosy presentations. Not just roads and transmission. Most plans to build carbon capture technology on power plants have failed before they ever started running. There are only four currently operating in the world, and they have been plagued by cost overruns, and operational problems that cause them to capture far less CO2 than initially planned. All things that we ought to think about before diving into a $4 billion publicly-funded project that can’t possibly be built quickly enough to impact our near term gas shortfall.

So I decided to do a better analysis.

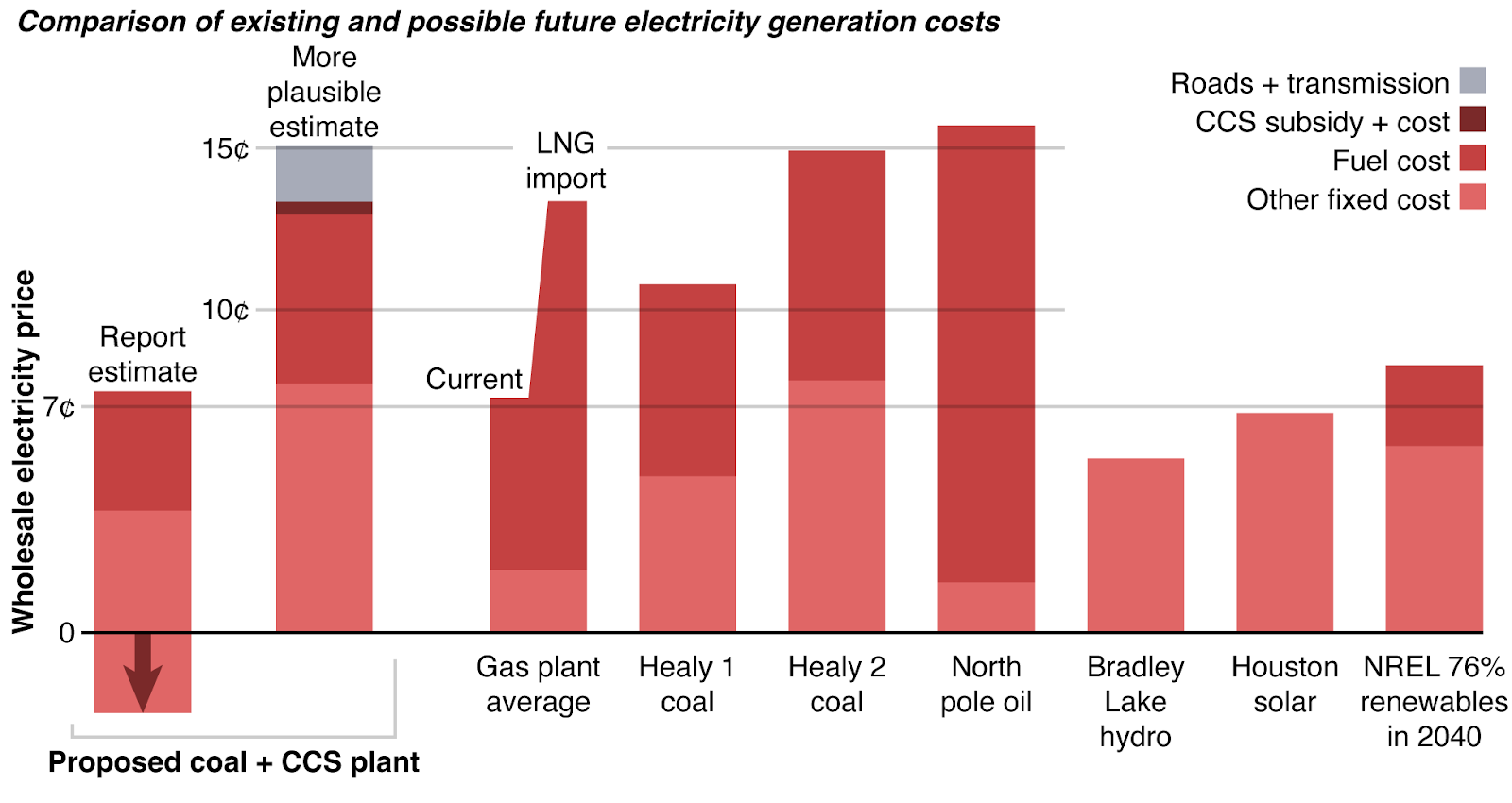

According to this feasibility study’s assumptions, federal tax credits subsidize the larger version of the coal plant enough to make it only a little more expensive than existing solar and gas generation, and slightly cheaper than the 76% renewable scenario in the recent National Renewable Energy Laboratory (NREL) report. According to more plausible (but still optimistic) assumptions, this plant will end up more expensive than gas power from imported LNG and far more expensive than the high renewable scenario, with carbon capture that’s likely to cost more than the tax credits will pay for.

What’s wrong with those assumptions?

Roads and powerlines are not free: They ignore all the costs of the road and transmission needed to actually connect this plant, 75 miles from the current electric grid. “The West Susitna Access Road is assumed to be funded by DOT and/or AIDEA.” And: “Power customers are assumed to permit and install their own power lines independent of this project. Such costs and permitting are not addressed in this study.” In contrast, renewable energy developers include the costs of power lines and substations necessary to connect to the grid in their power price. NREL includes those costs in its study. Ultimately, the consumers bear that cost.

They assume carbon capture and sequestration will work. Sequestering CO2 in a depleted oil or gas field is a relatively figured out problem. Capturing it from the exhaust of a power plant is not. Most proposed power plant carbon capture projects failed before they ever got started, the most egregious running up more than 7.5 billion dollars in costs (more than triple the initial estimate) along the way. There are only four such plants operating in the world. Two are recent pilot projects in China, without public data. The two in North America have a terrible track record. The Petra Nova plant in Texas aimed to capture 33% of emissions and actually got 27%, while the Boundary Dam plant in Canada aimed for 90% and averaged less than 60%, meeting its daily capture goals for only 3 days in the first 3.5 years of operations. Project proponents claim CCS at the proposed Susitna plant will operate at a never-before-seen success level, capturing 95% of emissions. If this plan runs into similar problems as other CCS operations, the federal tax credits won’t be enough to pay back the costs.

The fuel and power plant costs are wrong: The report not only fails to compare the coal plant costs to renewable power costs, it fails to compare them to power plant level costs at all. The only comparison they make is to a Chugach retail industrial rate that they pegged at 18.8 cents per Kwh, over twice actual power costs from current gas plants. For the coal plant, they assume capital costs vastly cheaper than listed in other Railbelt studies, coal prices significantly less than the Healy plants pay, and a capacity factor higher than any fossil plant on the Railbelt today. (see detailed assumptions at the end)

Adjusting any one of these assumptions to something more plausible bumps up the coal plant price to well above the 76% renewable scenario. Adjusting all of them bumps it well above even the costs of running gas plants on imported LNG, double the proponents’ estimate, and on par with the most expensive plants we use today. There are also some optimistic assumptions I didn’t change. I adjusted the capture success rate of the carbon capture plant, but left its costs as stated -- accuracy on those costs seems extremely unlikely for a technology with only two examples, neither recent. Experimental technology is rarely under budget. I also kept their assumption that the federal tax credits will last for the entire 30 years of the project, rather than the 12 years that is in current law.

Why are we talking about this at all?

My analysis above frames the question based on Railbelt power consumers. And from that perspective, it makes no sense to even consider this. If the question is “How should we power the Railbelt?”, it’s clear that even our not-so-good options (lots of imported LNG) are better than this, and our good options (mostly renewables) are vastly superior.

But the proponents of this plan may actually be answering a couple of very different questions: “How can we support a specific set of potential mines?” and “How do we take advantage of generous federal subsidies for carbon capture?”

The power needs of the proposed Donlin mine are mentioned many times in the report. Donlin is unlikely to be able to buy gas from Cook Inlet to supply its power.

Additionally, Flatlands’ energy’s coal lease is useless without a customer for the coal, such as this power plant. Coal hasn’t been exported from Alaska since 2016, and the Usibelli mine supplies all the existing coal plants. Other potential mines are one of the big drivers for the West Susitna Access Road. Cheaper solutions to the Railbelt’s power needs don’t do anything for these mine claim holders. But they would benefit if the public built them some infrastructure.

This plan is being promoted by the state’s CCUS working group. With half the members from industry, and the rest from governments and the university, it’s mission is to “accelerate commercial carbon capture, use, and storage (CCUS) projects within the state,” by means of finding a project that could potentially be funded by the new $85/ton carbon capture and storage tax credits. Having dismissed all of Alaska’s existing coal plants for not being in good carbon storage locations, and our gas plants for their too expensive fuel, it seems they felt their only option was to put a new coal plant somewhere close to storage. There is no “commercial carbon capture” for power plants.

What about the climate impacts?

The project proponents tout that a coal plant with 95% carbon capture would produce less than half the emissions of a natural gas power plant, at 0.2 metric tons per MWh as opposed to 0.44 (the current Railbelt total for all generation is around 0.5 metric tons/MWh). This is theoretically true, if such a plant existed. But neither of the two existing coal plants with CCS has come even close to capturing 95% of its CO2. One never aimed to capture more than a small fraction. The Boundary Dam plant that originally set its sights on 90% capture later changed its target to 65%. The plant’s recent emissions are 0.4 metric tons/MWh, and their reports have drawn the line of success as staying below the threshold to trigger a carbon tax. In contrast, the 76% renewable scenario would produce around 0.1 metric tons/MWh, less than half of that theoretical coal plant, and far less than any actual coal plant..

Of course, it’s true that any new technology starts out expensive and not working well. Some ideas will always fail, and some, over time, will improve. So there is a place for trying out CCS technology -- and that place is where there are already emissions. If you try this on an existing coal plant, and fail, at least the problem hasn’t gotten any worse. If you build a new one, you’re creating a brand new long lasting climate problem in order to maybe, partially, if you’re lucky, solve it.

The report throws out a few ridiculous calculations to supposedly make the plant climate neutral. One involves offsetting the climate impacts of vast fields of imaginary coal-heated greenhouses by piping in CO2 and waste heat rather than heating them with coal directly. Certainly one could reduce emissions by not burning coal in your greenhouses, but no such greenhouses exist so it’s hard to see how one would achieve an offset by reducing their emissions. Another involves burning beetle-killed spruce trees so they won’t slow down the growth of future forests, but there is no evidence (even in the citation provided in the report) that trees somehow grow faster if you cut down the dead trees next to them.

In Conclusion:

This idea has received far more press than it deserves, and is distracting from sensible near-term efforts to address the gas crisis, cheaper longer term solutions like the 76% renewable scenario, and current legislation to smooth the way, such as the bill addressing wheeling fees and tax structures for independent power producers. But even if it doesn’t make sense, it could still get built. Or at least cost a lot of money along the way to being abandoned (like many CCS proposals).

And if it does, one of the most worrying aspects about this expensive coal plan is that the costs and risks will fall on the public. Unlike renewable power projects, there are no independent power producer companies coming in wanting to finance and build this. There won’t be, because any such company would have to account for those cost risks, fund the infrastructure, and offer the utilities a firm, competitive, long-term price for the power. If this is built, it will be on our dime (the state and/or publicly-owned utilities). Right now, the university is asking for a $2.2 million grant match to fund the next piece of the study. It’s small, compared to the roughly $4 billion total cost, but it’s a small step in the wrong direction. There may be some stakeholders who benefit from this idea, but it’s not the Railbelt ratepayers.

Detailed Assumptions:

Road: West Susitna Access road costs from AIDEA. The Middle Susitna Skwentna option at $453 million is the only one that reaches the proposed mine/power plant area. I used half that cost, as the full proposed length goes farther than needed to reach the plant.

Transmission: Transmission costs of $17.7/KW/mile from the NREL study, doubled. 300MW is a large enough portion of the Railbelt load that it will need redundancy, to account for the contingency that a single line will trip and cut out half the Railbelt’s power. Similarly, the Susitna Watana hydro project modeled a triple circuit for that reason.

Coal plant

Size: The feasibility study highlights two proposed coal plant sizes: 400MW gross (300MW net with CCS) and 100MW gross (75MW net with CCS). While transmission is substantially cheaper for the smaller plant (and wouldn’t need a double circuit), everything else is more expensive, and it is less economic than the larger plant in both the authors’ and my analysis, so I don’t show it here.

Capital costs: The feasibility study uses capital costs of $5,572.5/Kw for the 400MW coal plant, while NREL lists $7,799/Kw, and the 2010 Black and Veatch Railbelt Integrated Resource Plan lists $10,109/Kw (when adjusted from 2009 to 2024 dollars). UAF’s recent coal plant using similar technology was constructed for $15,000/Kw. I used $7,000/Kw, in my analysis, which is still much more optimistic than all the other estimates.

Capacity factor: The study states that the new coal plant would have a capacity factor of 85%, which is much higher than any fossil plant on the Railbelt today (topping out in the high 60s/low 70s). I adjusted this to 75%, which is still higher than any current fossil plant on the Railbelt.

Fuel: They give coal costs at $3.50/MMBtu. I used coal costs equal to 2022 coal costs at the Healy plants of $4.98/MMBtu. It seems unlikely a new mine will be substantially cheaper than an existing mine, mining what the authors list as a similar coal deposit.

CCS: I used the overall CCS costs as stated, but adjusted the amount captured to 72% of their stated target, based on the average of the success (relative to targets) of Petra Nova and Boundary Dam, assuming most of the cost goes into building the facility, pipeline, and wells. This leads to a cost of $89.30 per Mt captured, slightly more than the $85/Mt tax credit. I did not adjust the capital cost of the CCS facility, even though any experimental facility is likely to come in over budget. I also kept the assumption that the tax credits, currently scheduled to expire in 12 years, will extend for the entire 30 years of the project.

Gas Plants:

Fuel: Current gas costs are taken from actual values from RCA filings for each power plant in 2022 -- the total amount paid at each plant for gas, including gas under Hilcorp contract and gas owned by Chugach. Imported LNG is modeled at $14/Mcf, with a gas plant efficiency of 8.2 Mcf/MWh, equal to overall efficiency of all gas plants in 2022. The NREL study lists gas costs at $12.1/Mcf, rising to $13.2/Mcf by 2040. I used the higher number as a more conservative estimate, to show how the coal plant compares to gas on the more expensive end of existing predictions.

Non Fuel: Non-fuel costs are derived by summing the “total production costs,” minus the fuel cost, for every gas plant on the Railbelt in 2022, from RCA filings. This number is divided by the total gas plant net MWh for 2022. This includes both regularly used and rarely used plants, and both fixed and variable production costs.

76% Renewable scenario: Total costs and fuel costs for the 2040 reference scenario of 76% renewables are from the graph on p 35 of the NREL report, divided by the total generation of 5941 GWh from p38.