Four years after Hilcorp’s announcement, are we solving the Cook Inlet gas crisis?

In May 2022, Hilcorp -- which provided around 80% of the gas for Southcentral utilities -- announced that it would not renew any of its Cook Inlet gas contracts. This should not have shocked anyone. While the exact timing of a crisis is hard to predict, the unsustainability of supplying a fixed market from a declining gas basin has been spawning concerning reports for nearly two decades. In 2018, the state’s report estimated that Cook Inlet gas could satisfy demand until around 2030, with prices to bring new supply online rising sharply by the late 2020s. This is not much different from what the state estimates today.

Nevertheless, the 2022 announcement was a catalyst of attention. The Cook Inlet gas crisis has been mentioned by nearly every energy news story, report, and energy-related piece of legislation for the last four years. Two years ago I laid out where we were, and where the crisis might be going. What has happened since then?

At the start of 2024, the utility working group was focused on building import facilities ASAP for a possible 2027 shortfall. By the beginning of 2025, the utilities had gone separate directions, with Enstar signing an exclusivity agreement with Glenfarne on a plan tied to the AKLNG proposal, while CEA decided to work with Hilcorp on reopening the old export terminal as an import terminal.

In 2025, the timeline got stretched. Utility use dropped by around 8%. Most of the savings were from cutting off gas power to Fairbanks, which replaced it with coal and oil power, while some was due to a shift from MEA’s less efficient gas plant to CEA’s more efficient plants. Heating consumption was also below average. Starting in October, the Fairbanks gas utility switched to using trucked North Slope gas.

Furie was able to supplement the Hilcorp contracts with discretionary gas, but at a substantially higher price. The state’s new estimates show a small amount of extra production in the near term and reliance on stored gas in later years, with a new running-out-of-gas estimate in 2033. In the meantime, nearly all the major renewable power proposals on the Railbelt were dropped, no clear decision was made on any import plan, and the gas line reentered the conversation.

In 2026, the gas line has completely dominated the conversation. The two-phase nature of the current iteration of the gas line means that the pipeline itself has to be financed on the backs of in-state gas customers. This relies on two things that don’t go together -- a significant price hike and a large increase in in-state demand. Imports are still in all utilities’ written plans, and the Regulatory Commission has an open docket on whether it really makes sense to have two or three separate import projects in Cook Inlet. Despite all the talk, the gas line probably won’t happen.

Meanwhile, early 2026 was cold, and some of the extra gas pushed into storage got pulled right back out again. The price of new Cook Inlet gas is around 50% higher than old contract prices, and in March Hilcorp sold emergency gas to Enstar for nearly double the old price.

This is feeding into both electric and heat bills. Enstar’s price to households has risen around 30% since Hilcorp’s original announcement. GVEA recently raised the fuel portion of its rates by over 60% in a quarter -- adding around $46/month to customers’ bills. Overall, all utility rates have risen faster than inflation since the Hilcorp announcement.

Cook Inlet Gas is squeaking along for a few more years, but the new gas is a lot more expensive

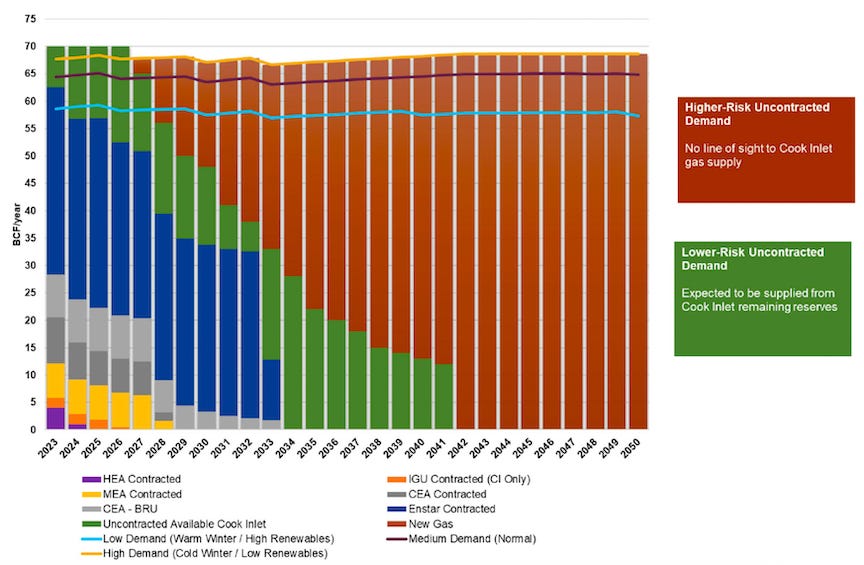

In 2023 a consultant hired by all the utilities came out with a graph showing a potential shortfall in 2027. However, even in their “high demand” scenario, there is extra gas in early years which can potentially be stored.

Also, while Cook Inlet in total has been producing and consuming around 70 BCF (billion cubic feet) of gas each year, only around 60 goes to gas and electric utilities, with the rest used in field operations and industry. Looking only at utility use, and updating the graph based on RCA filings, you can see that most of that green ‘uncontracted available’ in the near term is now filled in with contracted Cook Inlet gas. And while some of that 2025 dip comes from weather, most of it comes from more durable changes -- not selling gas power to Fairbanks, the Fairbanks gas utility switching to buying trucked gas from the North Slope, and greater power pooling in the central region.

Updated based on RCA filings. Time periods beyond filed projections and contracts are equal to the old graph. Enstar’s contracts include 3.2 BCF of Bluecrest gas in 2026-27 it referenced in its latest gas cost adjustment.

The “little bit further” contracts:

The remaining gas buyers are going with a ‘stretch the timeline’ strategy, sticking gas in storage or trading gas now for gas later to try and make it last a little longer. While the original Hilcorp contracts end in 2028 and 2032, the utilities now believe they can stretch their gas to 2029 (MEA), 2030 (CEA) or 2033 (Enstar, currently including HEA).

CEA has agreements with Hilcorp and the Tesoro refinery which allow it to give those companies extra gas today in exchange for 80% of that gas volume in future years (CEA owns a large part of the Beluga River gas field, which is currently producing more than CEA uses). MEA does not own a gas field, but has made a similar agreement with Hilcorp. Instead of exchanging gas it owns, it exchanges the headroom in its Hilcorp contract -- the gas it’s entitled to buy but does not need -- getting it back at the end of its contract term. In exchange, it’s forgone the last two years of under $8 gas in the contract, paying $9 and $10.25 instead for those two years, and $11.75 for the added year of extra gas.

Non-firm gas is a growing and expensive part of the mix

While CEA and MEA have moved gas around to get a little bit more from Hilcorp, Enstar has filled in the gaps with non-firm contracts.

From 2022-2024, Enstar bought more than 95% of its gas through firm contracts. In 2025-2026, this dropped to 86%. The remaining gas is bought through short term contracts that don’t have volume guarantees and don’t go through regulatory review. These prices can be changed much more frequently. Most of this discretionary gas is being sold at around $12-14/MCF, and Enstar expects this share to grow, providing around 20% of the gas in its next forecast period.

In recent years, all of this more-expensive gas has come from Furie, but Hilcorp is now also providing some gas at similar prices, as well as their $16 emergency gas.

Meanwhile, newer firm contracts look more like the variable ones, both in price and uncertainty. Enstar’s five-year Furie contract starts at $12.30/MCF and has a list of ‘development milestones’ that might impact the amounts they can actually deliver. One such milestone (getting a new jack-up rig into Cook Inlet) has already been missed.

Gas Storage

Storage is an integral part of the plan to squeeze the last bit of gas out of Cook Inlet -- with both producers and purchasers getting gas whenever they can and holding it underground to be released precisely when the utilities need it. That doesn’t always show up directly in the gas price -- but it adds costs. Both CEA and MEA have contracted for new storage with Hilcorp. Hilcorp has added a (currently disputed) storage fee to some of the gas it sells to Enstar, on the grounds that the storage is a necessary component of delivering it. Enstar has expanded its storage facility at CINGSA, and has asked the RCA for preapproval to build a new $240 million storage facility.

A longer timeline

Also see the regularly updated Cook Inlet Gas Dashboard.

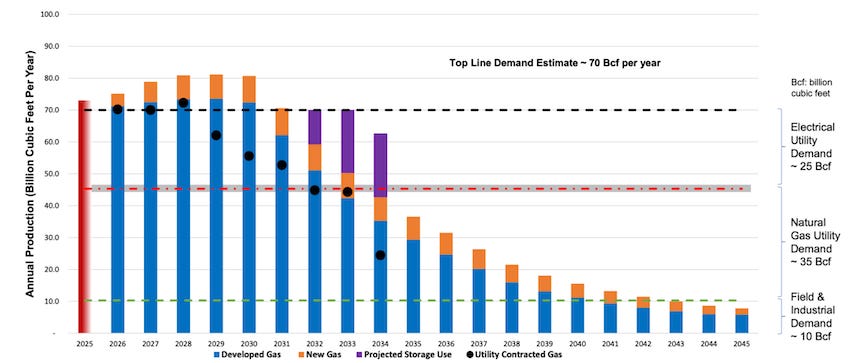

Put that all together, and you get the new estimate of 2033. But the electric utility demand in this graph still includes the gas power Fairbanks used to buy, so it could even be a little later. This has thrown us out of a “let’s all work together as quickly as possible” scenario and into a war of competing ideas with three possible import plans and an in-state version of a gas line all claiming that they can be the solution.

Warring import plans

2033 still isn’t far away, and imports are still the most likely scenario.

After Hilcorp said it wouldn’t sign new contracts in 2022, all the utilities got together, hired a consultant, and started working on import plans. In fall 2024, that alliance fell apart, when Chugach Electric (CEA) and Enstar decided to go different ways. CEA has partnered with Harvest (a Hilcorp subsidiary) on a plan to refurbish the old export terminal in Nikiski to be an import terminal. Enstar has partnered with Glenfarne on a plan to build a new import facility in conjunction with (and sharing some facilities with) the proposed export facility for AKLNG. Cook Inlet Energy was working on its own plan in the meantime to construct a floating facility in Cook Inlet using the infrastructure from the old Osprey oil platform, and went public earlier this year -- saying it will partner with any gas buyer that’s interested.

The Regulatory Commission of Alaska is concerned that customers will end up stuck paying unreasonably inflated infrastructure costs to construct multiple facilities for a single small market, and have ordered CEA, and Enstar to file hundreds of pages of information justifying why their plan is best. “Both utilities have also told us, in -- in their opinion, that it would be in the best interest of consumers that the utilities pursue these projects together rather than independently, because to do so would reduce consumer costs on an overall basis and potentially avoid the necessity of seeing duplicate facilities.” (docket I-26-001)

CEA claimed that according to the information they have, their project with Hilcorp is cheaper and will produce cheaper gas for customers. Also that by starting small (the imports would start at 20 BCF per year with options for expansion), it allows flexibility depending on how much is needed. They haven’t signed any binding commitments yet, and wouldn’t own the facility.

Enstar did NOT claim that its project is cheapest. Instead, it carefully claims that the Glenfarne project beat the other top project in “three of the four highest-priority metrics” (only one of which is delivered gas cost), while coming out worse on “Project Complexity and Integration” and “ Size of direct investment required by the utilities.” Delivered gas cost isn’t necessarily the other metric Glenfarne failed on, but Enstar didn’t specify, and investment cost is certainly linked to gas cost. Instead, Enstar is focused on the ability to pivot to using North Slope gas from AKLNG if it comes online, which “minimizes the “Regret Costs” that could be realized. Although not a part of the formal scoring criteria, this was important to ENSTAR.” They anticipate being able to bring in their entire gas needs right away.

Enstar has signed a binding commitment with Glenfarne, and will have to pay Glenfarne $43 to $48 million if the project is canceled. Enstar tried to get pre-approved to charge this cancellation fee to customers in gas rates. The RCA told them no -- but they can come back and ask later if it happens. Enstar’s CEO has also said that Hilcorp’s involvement is a deal-breaker for them, regardless of other factors. “I made it very, very clear statement to this group that there is no world in which ENSTAR will participate in a project that has a Hilcorp owned entity as the importer of natural gas.” Which more or less sounds like ‘we’ll coordinate if you join our plan, but not otherwise.’

And although Glenfarne is still supposedly working on this import plan with Enstar, and Enstar still has an “import phase” in their presentations. Glenfarne itself never mentions it and claims they will have a pipeline by 2029, which would likely obviate their need to build one.

Cook Inlet Energy claims its use of existing infrastructure is a big advantage over older floating storage and regasification plans, and promised to compare their proposal to the ones laid out in the consultant reports. They think their project is feasible at 22 BCF per year, but that it could be expanded to meet all of Cook Inlet’s needs. I asked Cook Inlet Energy directly if the other two projects had to fail for theirs to succeed and they seemed to think it was possible to coexist with the Hilcorp/CEA plan.

Complicating things further, the RCA can’t actually regulate import facilities at all, but only threaten the utilities that it won’t allow them to get back their costs in rates if they do something unwise.

After an initial rush of filings in that docket, the import news has gone quiet in favor of gas line chatter.

An in-state gas line would lead to expensive gas, or more likely none at all

This is still the least likely solution, despite all the attention. Glenfarne’s current iteration splits the project into two phases. An in-state phase 1 where a giant line supplies a relatively tiny amount of gas to local customers, and a phase 2 export plan.

The large export plan isn’t a solution to Alaska’s near term local energy shortage because it relies on outsiders to make it happen for us, with no guarantee they’ll decide to do so now, when they have not decided to do so any time in the last 40 years.

The in-state gas line is incredibly vulnerable both to cost overruns and to gas consumption volume. It takes magical thinking to make it pencil out without the exports.

Pipeline prices depend on volume

To explain, Cook Inlet currently has expensive gas, and relatively cheap distribution infrastructure. This is why Enstar heat bills actually compare somewhat favorably to gas bills in other places.

When we’re thinking about imports, the basic drivers are the same, albeit more expensive. Most of the price would be the gas cost and shipping cost, with the infrastructure adding a few dollars to the price (maybe more if we end up with 2 or 3 import terminals).

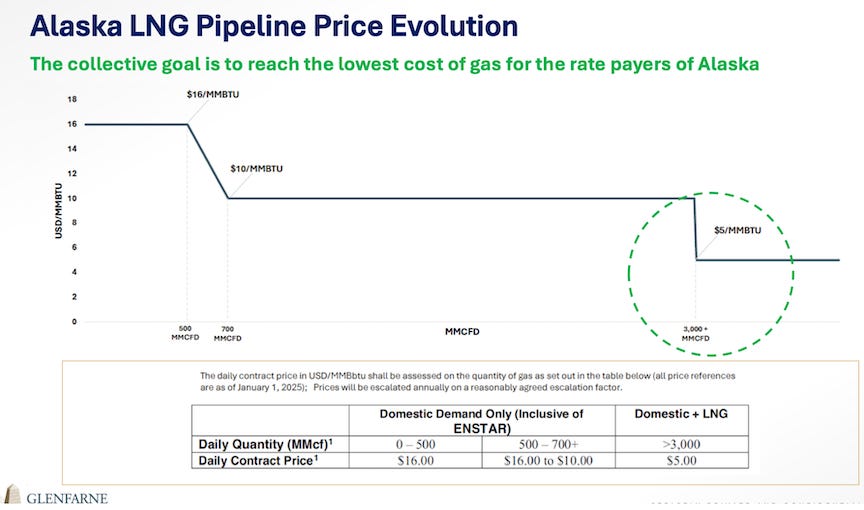

An in-state gas line would reverse that completely. The gas from the North Slope is expected to be relatively cheap, but the pipeline to deliver it would be very expensive. If you sell a lot of gas, those pipeline costs get spread out over many customers (the export scenario). If you sell an Alaska amount of gas, the local customers have to pay for a $15 billion pipeline with their rates.

Because of this, no one has even done the math on a scenario where gas demand doesn’t increase dramatically. Even the outrageously expensive estimates benefit from a massive growth in local gas use. The increase isn’t usually explained, and often isn’t even mentioned. Yet new industrial gas users are very unlikely to be attracted by gas prices much higher than today’s already high prices.

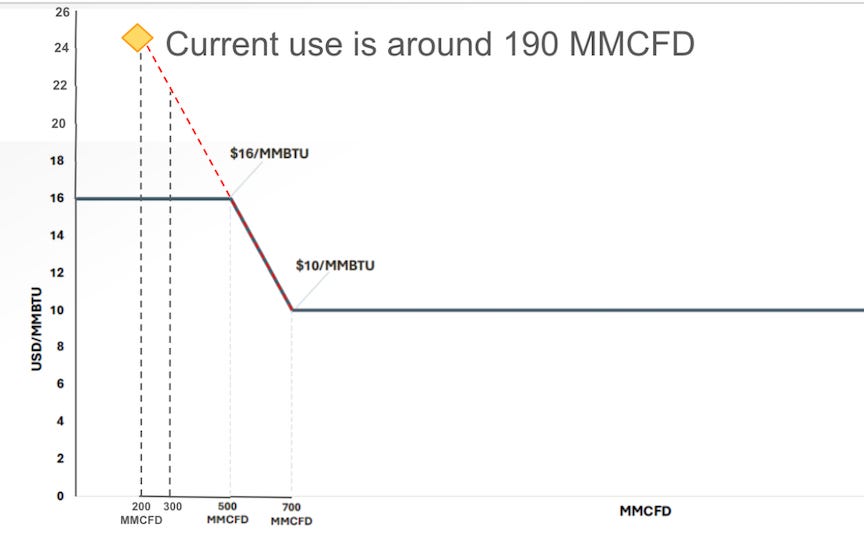

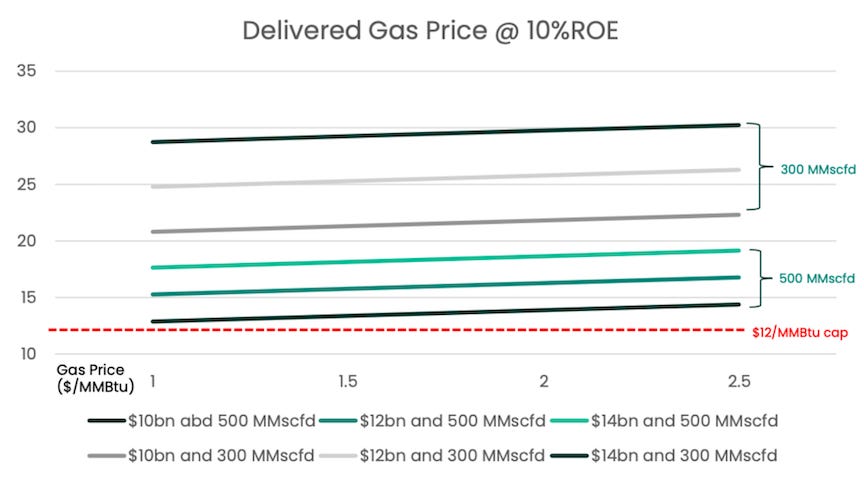

Glenfarne’s most recent graph illustrates a price vs volume relationship from a starting point of 2.5 times more use than Cook Inlet today.

But the actual problem is much worse. It shows a theoretical price drop at the point where use is more than 3.5x today’s use. If you continue their line off to the left until you hit actual current consumption, it suggests the price at that level should be over $24. Glenfarne claims that they’ll lock the price at $16 plus inflation. Since that would be a money-losing proposition at current volumes, keeping such a commitment would likely be impossible without new industrial customers willing to sign long-term contracts for >$16 gas. They claim that they could make the math work with only 1.4-1.7x current demand, but that’s still a lot.

The other analyses of the in-state price show the same thing. The state’s consultant calculates that if the pipe comes in on the low end of Glenfarne’s range estimate, with the cheapest possible gas price and nearly 3x current demand, that could lead to a price in the $17-$18 range. But if there’s only 1.7x current demand it jumps way up to almost $30 at the low end. Actual current demand isn’t even modeled.

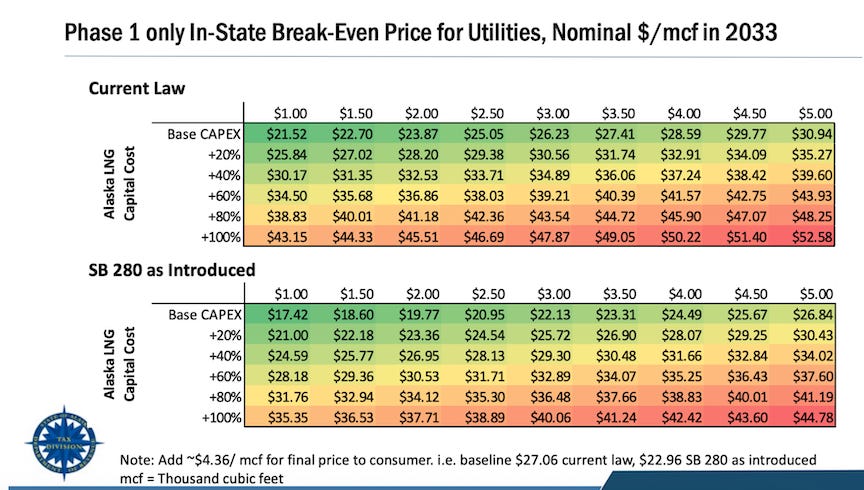

The state Department of Revenue tried to solve this in a different way, assuming that you bring in a large industrial customer to nearly double what utilities use, and charge them much less ($6/MCF) than what you charge the utilities. Even with that, utilities end up paying more than $20/MCF, and possibly much more (Glenfarne’s latest cost estimates put the pipe at +14% to +45% capex). Also, $6/MCF is likely too high to attract a location-independent user.

If you build it, why would they come?

The gas line idea has to hope for two sets of customers to appear, first, the in-state customers who will buy enough gas prop up the $16 price, and next, the export customers who will finance the rest of the project.

The set of customers who might want to buy gas at double the price that drove the fertilizer and export facilities to close is likely limited to those who are A: geographically stuck, and B: only have more expensive options. This eliminates any location-independent industry, and leaves you pretty much with just Donlin Mine and Fairbanks (plausibly around 1.3x current demand). They aren’t enough. And working in the opposite direction, current customers will have a lot of incentive to buy less gas at those prices.

Enstar’s heating customers would have a huge incentive to conserve -- Enstar mentions potential conservation due to high gas prices as a business risk in its rate case to justify a high rate of return. And non-heat users would have even more options. Electric utilities buy about a third of Cook Inlet gas today. Electricity can be produced from many sources, and the more expensive gas is, the more attractive the other options are. At $16 gas, even the diesel and coal plants will be competitive with gas plants in some years. An import facility could get built as competition. An electric utility would be crazy to sign a 30 year $16 contract -- and that goes for GVEA in Fairbanks as well.

Importantly, none of this changes the fixed costs of the pipeline, which still have to be recovered, so each drop in use would make the gas more and more expensive for the remaining users, or lead to the complete bankruptcy and shutdown of the project (if the prices really are fixed).

All the players know this, and what this likely means is that even if Enstar does sign a contract for it’s current demand (which it may not be able to sell at those prices), that’s not enough to fund it, and the in-state line won’t actually happen unless the big export plan is happening, which puts Alaska in the same place it’s always been. Waiting for outsiders to save us is not an energy plan.

Imports vs. Cook Inlet vs. Gas line -- what will it all cost?

When I posted two years ago, the predicted prices for imported gas ranged from $12-$16. Adjusted for inflation, it’s still pretty much the same. If you adjust the prices for new Cook Inlet gas for inflation they also end up in that range.

The in-state gas line wouldn’t be cheaper. There’s a much-repeated claim that Enstar/Glenfarne’s proposed $16 in state gas line price would be cheaper than imports. This comes from the state escalating an old import figure to 2033 dollars and ending up with “about $17.” But the $16 ‘cap’ is subject to inflation, and will be more than $17 by 2033. In the best case for the line, they’re similar. In most projections, imports are cheaper.

Imports and potential exports are part of the same market. No one can predict prices, but the same predicted global LNG glut that makes the economics of the export gas line so dicey (with a 20% increase in capital costs pushing it into uneconomic range), would also suppress import prices. Brad Keithley’s analyses show in-state gas line prices substantially more expensive than imports.

Meanwhile, since the original Hilcorp announcement, all utility rates (combining base rates, fuel rates, and customer charges) have been increasing faster than inflation, which is likely to continue.

What Next?

It’s good that we’re unlikely to run out of gas next year, but not great that we really haven’t fixed the problem. Import facilities and reducing gas consumption are still the only solutions within local control. And the cost of doing nothing at all is still enormous. If we do nothing, we might pay $25-$30 per Mcf to ship in gas in little containers, or the $40/MCF from Enstar’s pilot project trucking gas from Canada -- which couldn’t even scale up sufficiently.

Two years ago I said “Someone should probably do something. Specifically, Enstar should make a final investment decision on an import facility, all the Railbelt utilities should sign contracts for large scale solar and wind facilities, and the rest of us should make our buildings more efficient.”

Someone should still probably do something. Enstar is contractually bound to work only with Glenfarne, so will presumably have to wait to see if Glenfarne commits to either the gas line, the import facility, or neither. HEA is too small, and also contracted to get its gas from Enstar until 2031. The best someone to do something is probably CEA, possibly with MEA or GVEA as well -- they’d be enough to drive one of the two smaller import plans forward.

All the electric utilities should work to use less gas. While the Railbelt energy system has been quite static for the last decade, the rest of the world and country has leapt ahead on integrating different energy sources. Most of the large-scale solar and wind contracts that were being discussed two years ago have since died, but there are smaller projects still in the works that should still move forward, including solar, wind, and hydro. Meanwhile the integrated resource planning process is ongoing, and will hopefully help point out good larger projects that will benefit the grid as a whole. (I’m part of the preferred portfolio working group for the IRP -- so at least I’m hoping it’ll come up with good ideas).

And building energy efficiency is always a good idea. In the past the state has funded weatherization and efficiency. It should do so again.

In two years I hope we have a real plan.In two years I hope we have a real plan.